At some point in midlife, many women experience a very specific kind of financial awakening. It usually arrives quietly, perhaps while reading an article about retirement, overhearing someone mention Social Security, or realizing your children now know how to explain cryptocurrency but still can’t remember to replace the toilet paper roll.

Suddenly, retirement doesn’t feel abstract anymore. It feels close enough to make eye contact. Iif you’ve looked at your savings and thought, Well, this seems less “golden years” and more “aggressively behind years,” you are not alone.

Many women over 50 are trying to make up ground financially, often for reasons that had nothing to do with irresponsibility. Careers were interrupted by caregiving. Marriages ended. Parents needed help. Children needed support. Some women earned less for decades while doing more. Others simply spent years putting everyone else first because that’s what women were quietly expected to do.

So before anything else, let’s clear something up: feeling behind does not mean you failed. It means life happened. And life, unfortunately, has never once consulted a retirement calculator before creating chaos.

The good news is that catching up is still possible. Not through panic, deprivation, or becoming one of those people who suddenly starts using phrases like “wealth mindset” on social media. Just through practical, steady adjustments that improve your future without making your present miserable.

Stop Comparing Your Retirement to Someone Else’s Fantasy

One of the first things that helps is redefining what retirement actually means to you. We’ve all seen those terrifying headlines insisting you need several million dollars to retire comfortably, preferably while standing on a yacht wearing linen. But retirement is not one universal experience. Most women are not aspiring to own a vineyard in Tuscany. They want stability, freedom, and a home they can afford. Enough money to enjoy life without constantly worrying about every unexpected expense.

Retirement planning becomes much less intimidating once you stop comparing yourself to fantasy lifestyles designed by financial marketers and cruise commercials.

Face the Numbers Without Judging Yourself

From there, the next step is honesty, not doom-filled catastrophizing. This means sitting down and looking at your numbers. Retirement accounts, debt, monthly expenses, savings, and projected Social Security benefits. Not because you need to punish yourself, but because clarity is always less frightening than avoidance. Financial uncertainty grows in the dark. Numbers may not always be comforting, but at least they are concrete.

And no, discovering you should have started saving more aggressively in 1998 is not useful information now. If we could all go back and make perfect financial decisions, most of us would also have bought Apple stock and used sunscreen more consistently. What matters is what you do next.

Small Financial Changes Still Count

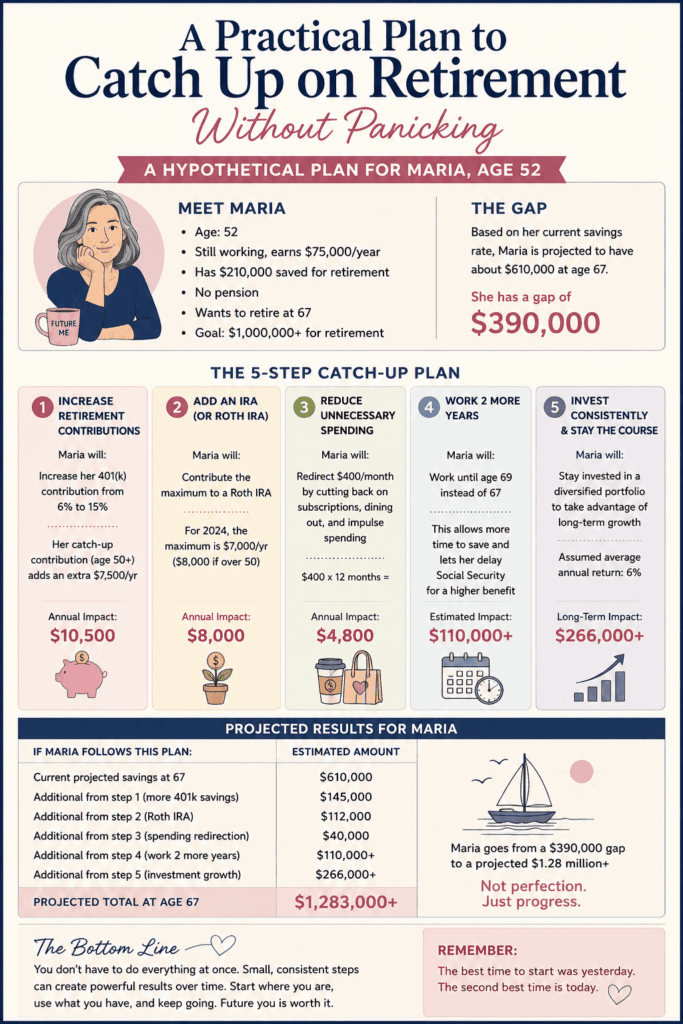

For women still working, this is often the season when earning power is finally stronger. Children may be grown, careers may be more established, and fortunately, retirement rules recognize that many people need extra time to build savings. Catch-up contributions allow those over 50 to put additional money into retirement accounts, which can make a meaningful difference over time. Even increasing contributions modestly can help more than people realize.

Notice I said modestly. There’s a tendency to think financial improvement only counts if it’s dramatic. But retirement security is usually built through consistency, not heroics. A little more is saved each month. A little less wasted on things that don’t truly matter. Small corrections repeated steadily over several years can completely change the trajectory of your finances.

Be Honest About Where Your Money Goes

By this stage of life, many women know exactly where money mysteriously disappears. It leaks into subscriptions nobody uses, impulse purchases made during moments of stress, and the ongoing financial support of adult children who somehow still need help despite being fully capable of explaining TikTok algorithms.

This is where things can get emotionally complicated. Women are often conditioned to prioritize everyone else’s needs first. But retirement requires acknowledging an uncomfortable truth: no one is coming to rescue your future self financially. At some point, protecting your own stability becomes not selfish, but necessary.

Retirement Doesn’t Have to Look One Certain Way

Another important mindset shift is letting go of the idea that retirement must happen at one precise age or in one specific way. The cultural image of retirement still tends to involve abruptly stopping work forever and immediately taking up golf. But increasingly, many women are creating flexible retirements instead. Some continue working part-time. Others consult, freelance, teach, or pursue passion projects that bring both purpose and income. Sometimes working a little longer is not a failure; it’s simply strategic.

Simplifying Can Be Surprisingly Liberating

Housing also becomes part of the conversation eventually. Downsizing has long been treated like a depressing rite of passage, but for many women it can be surprisingly liberating. Less maintenance. Lower expenses. Fewer rooms to clean and fill with decorative pillows nobody is allowed to touch. Simplifying life financially often creates emotional breathing room too.

Don’t Let Panic Make the Decisions

Perhaps the most important thing, though, is resisting panic itself. Panic is expensive. It leads people to make impulsive decisions, avoid looking at finances altogether, or assume it’s too late to improve anything meaningfully.

In fact, some of the most financially stable retirees are not people who earned extraordinary incomes. They are people who became intentional. They adjusted, planned, and stayed flexible. They made reasonable decisions consistently over time instead of chasing dramatic financial transformations.

That’s the part nobody glamorizes because it’s terribly unsexy. There are no inspirational montages for “finally understanding your monthly spending habits.” No one makes movies about increasing IRA contributions. Yet those ordinary decisions are often what create security later.

So if you feel behind, take a breath, not a panicked one, just a normal adult breath. You do not need to solve your entire future this week. You simply need to begin where you are. Open the account. Review the budget. Ask questions. Make one smart decision, then another.

Read Next: